Last Friday, the Russell 2000 - the small-company index - had a decent rally. If you look closely at the chart above, you can see that Friday erased Thursday's losses. Good news, right?

Well, take a look at the lower panes. Specifically, take a look at that red circle. That is the 14-period RSI. When RSI gets down to that green line, which is set at 30, that traditionally implies that the security is "oversold". In plain English, the implication is that it has gone too far, too fast. What frequently - but not always - happens is we see an "oversold" bounce. We could easily argue that's what happened on Friday. The bottom pane is the MACD indicator. Since these articles are intended for the average American, not the technician, here's the point: When I look at these three indicators together, in my view, it confirms that Friday's price move was just an oversold rally.

More importantly, that also implies that the selling pressure is not likely to be over.

This coming week is Thanksgiving week. This week typically sees very little volume of trading. So, any move will be suspect in my view unless it carries very high volume.

Here's my concern, at November's outset, I produced our monthly video analysis for our YouTube channel. In that video, I stated that I do not believe we will see a recession in the near term. Since then, I'm losing that confidence.

For context, know that the Atlanta Federal Reserve's GDPNow tool is suggesting that third quarter GDP was ~4.2%. If that stat is accurate, that will represent fantastic growth last quarter. Meanwhile, the NY Federal Reserve's GDP Nowcast is forecasting ~2.3% for the third quarter. If the NY Federal Reserve's estimate is more accurate, it will still represent pretty solid growth.

But both stats are historical. They are in the past.

The stock market, on the other hand, is a future discounting mechanism. It has historically gone down before a recession starts. The challenge, of course, is that there are many small and minor stock market corrections that do not lead to a bear market and do not actually forecast a recession.

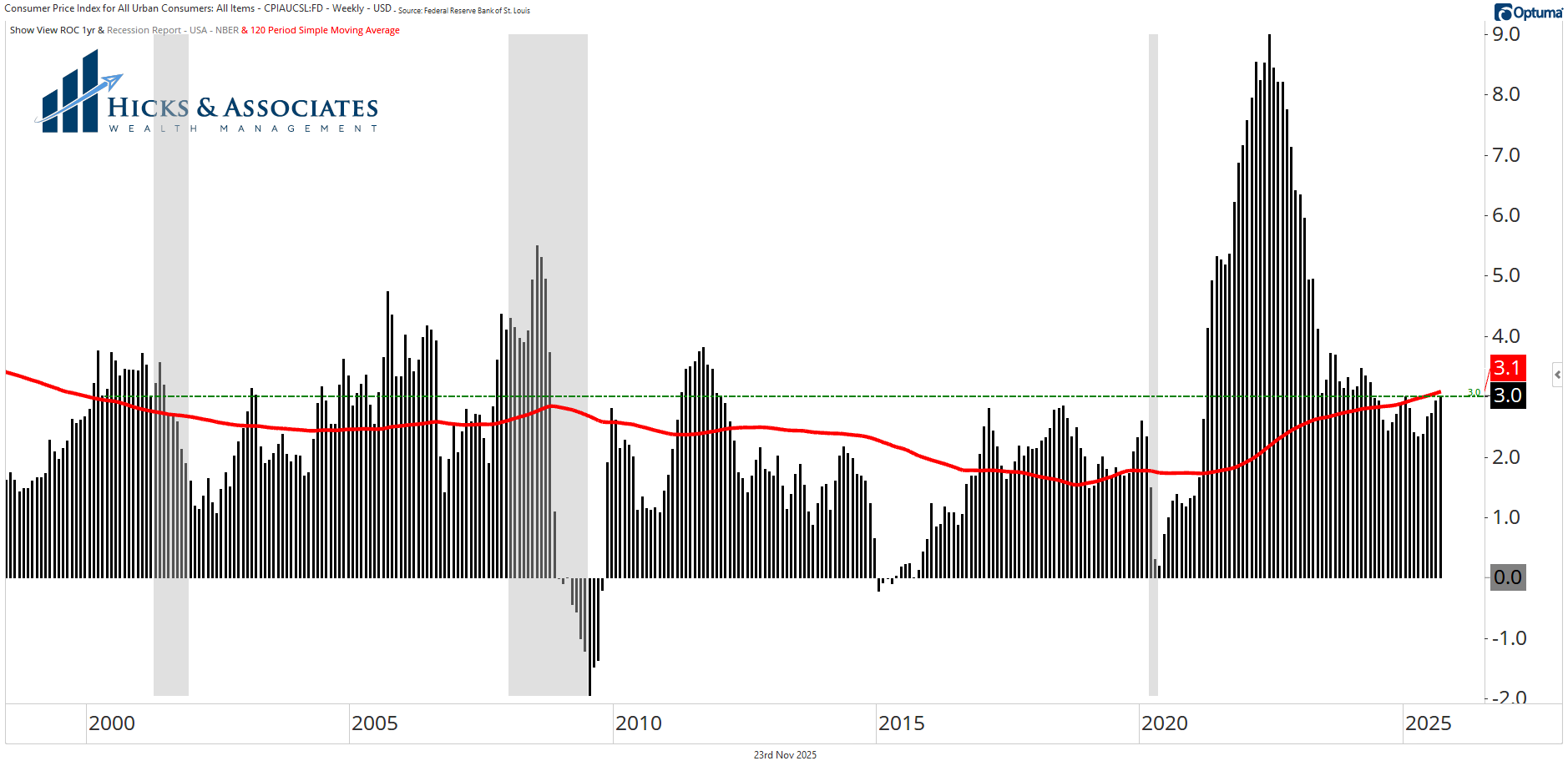

Before sharing my final concern, take a look at this chart for inflation over the last twenty years.

This is the Consumer Price Index. Each vertical bar represents a month's year-over-year change. The red line is the ten year average. We all remember the massive spike in inflation right after Covid. Since then, the Federal Reserve has been fighting inflation and trying to bring it back under control - to the extent that they have any.

Unfortunately, the last five months in a row, CPI has ticked higher. The last update has CPI at 3.0% and the ten-year average is now at 3.1%. The problem is that the Federal Reserve has a stated goal of 2.0% inflation. From what I understand, this 2.0% target is completely arbitrary, but space is too limited to go into that detail. For now know that they allegedly want to get to 2.0%.

Here's the problem:

While I do still believe it is possible we will avoid a recession, I also believe that the economy is very finely balanced right now. From what I see, our economy could easily tip into recession. This is why, in my view, the Federal Reserve has been right to start lowering the Fed Funds rate. Unfortunately, it appears that they might be done lowering rates for now. They may not lower rates again next month because they are worried about inflation continuing to tick higher. But look at that chart above. First, there are plenty of times when CPI has been higher than 3.0% (denoted by the green horizontal line). Second, the ten year average is 3.1%. So, do we really need to get inflation down to 2.0%? Inflation is not that bad. No, prices have not come down - that's deflation and you don't really want deflation. Ultimately, right now, inflation is not that bad.

But if the economy is finely balanced, further interest rate cuts would help stave off a recession.

My fear is that the Federal Reserve is willing to risk a recession in order to get down to a target that I'm not convinced is really important.

PS. The tariffs have also not helped. But that's a whole 'nother article.

This information is intended to be educational. Hicks & Associates Wealth Management does not provide tax or legal advice. You should consult with a qualified tax, legal or financial professional before making any decisions.

Investment advisory services are offered through Hicks & Associates Wealth Management, LLC (“Hicks & Associates”), an investment adviser registered with the Securities and Exchange Commission. Registration as an investment adviser does not imply a certain level of skill or training. More information about Hicks & Associates can be found in Form ADV Part 2 or Form CRS which is available on our website.

Past performance is no guarantee of future returns. Hicks & Associates reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The visuals shown are for illustrative purposes only and do not guarantee success or certain level of performance. This material contains projections, forecasts, estimates, beliefs and similar information (“forward looking information”). Forward looking information is subject to inherent uncertainties and qualifications and is based on numerous assumptions, in each case whether or not identified herein.

This information may be taken, in part, from external sources. We believe these external sources to be reliable, but no warranty is made as to accuracy. This material is not financial advice or an offer to sell any product. There is no guarantee of the future performance of any Hicks & Associates portfolio. The investment strategies discussed may not be suitable for all investors. Before investing, consider your investment objectives and Hicks & Associates charges and expenses. All investment strategies have the potential for profit or loss.